When you are beginning to dream about your first home, it’s easy to get carried away with yourself as you picture what home you will buy. When my wife and I started thinking about our future home, we started to confuse needs with wants. It started out with needing two bedrooms and one bath; you know, the bare essentials. Then, we started talking about where to have our office if we would have a guest bedroom. Before you know it, we’re adding on a third bedroom, a second bath, fenced in back yard (of course for our cute dog), and so on. It would be accurate to say that the conversation drifted from talking about our first home to our dream home.

If you are buying your first home, you have to be careful about buying too big of a house. Buying too much house is not only common these days, but also disastrous for your finances. Financial experts know and understand this reality – and in an effort to help, they’ve come up with simple calculations to determine how much house you can afford. Let’s take a look at these calculations, before I offer my own solution.

Popular Calculations to Determine How Much House You Can Afford

Everyone has their own advice on what you should be able to afford. Here’s some of the popular ones:

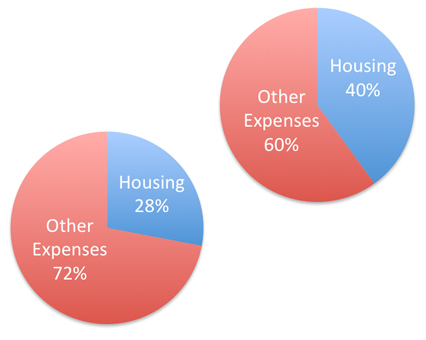

28-40% of Monthly Income

One rule of thumb is that you can afford 28-40% of your monthly income for your housing costs. In fact, many lenders use this as a limit for establishing how much they will lend you. This means that if you are earning $10,000 you can afford to pay somewhere between $2,800 and $4,000 each month on your house and related expenses.

1.5-3x Your Annual Salary

Another popular number that is thrown around is 1.5x-3x your annual salary. If you are earning $100,000 each year, that means you can afford $150,00-$350,000 in a house.

These are just some of generalizations that help you determine how much home you can afford and they should be treated as such. While they may be helpful, they fail to take into consideration the true costs of owning a home and your current budget. You cannot rely on these estimates if you are looking to buy a home. Doing so may lead you to foreclosure or something even worse.

Expenses with Buying a Home

In order to better assess whether you will be able to afford a house, or how much of a house you can afford, you first need to understand the number of expenses that buying a home entails. It’s not the same as renting. You don’t just have a monthly payment anymore like you would if you were renting.

- Down Payment – One of the first costs that you will incur when buying a home is the down payment. Usually lenders will require 20% of the home value as a down payment, especially if you want to avoid mortgage insurance. While it is possible to buy a home with less down, usually this comes with additional costs.

- Closing Costs – These are often the fees that are overlooked when buying a home, so first time home buyer is usually forced to empty any and all emergency funds at the last minute. These fees will include (but are not limited to): escrow fees, legal fees, inspections, prepaid loan interest, and more.

- Homeowners Insurance – Homeowners insurance is usually an additional few hundred (or maybe thousand) dollars each year, depending on the value of the home and location. Usually this is a requirement to get the final approval for the mortgage from the lender.

- Taxes – One of the additional costs that homeowners occur is property taxes. These will vary depending on the property value and the location of the property, you must account for these additional costs.

- Maintenance – Maintenance may be difficult to predict, but some say that you should budget for 1%-3% of the property value for maintenance. Some years will be less and some more. Regardless of the amount, you can bet on one thing: repairs are necessary.

- Monthly Mortgage Payment – Last but certainly not least, is your monthly mortgage payment. This will depend on the amount of the loan, the interest rate, and the duration. While you may initially aim to match the amount you are paying in rent, considering all of your other costs, you should probably look to have a lower mortgage payment than your rent.

Other Factors that Affect Your First Home Budget

Estimate how much house you can afford isn’t simply adding up all the costs and seeing if you have that much in your monthly cash flow. There are many other important things to consider.

- Retirement Planning – Do you have big retirement goals? Are you trying to max out your Roth IRA each year or maximize your 403(b) contributions? Buying too big of a house may put these goals on hold for years, if not decades. Make sure to consider your retirement planning and don’t assume that buying a home is ultimately the best thing for your retirement goals.

- Other Debts – People who have lots of consumer debt should not be thinking about buying a home. Before you even think about buying a home, figure out how much debt you have and what you can do to lower your debt. Not only will this lower the risk involved in buying a home, but this will increase your monthly cash flow thereby allowing you to pay for all of the expenses mentioned above.

- Children – I can’t stress the importance of this enough! If you are thinking about having children soon, you need to take that into consideration. Will it prevent one of you from working? If so, make sure that either you save up enough money to afford it or buy a significantly smaller home.

The Most Accurate Way to Calculate How Much House You Can Afford

While it may not be the most succinct answer to the question of how much house you can afford, below is the most accurate way to determine if you can afford a home. It’s not an exact science, and that is why you won’t see any numbers, ratios, etc. Follow these steps, be honest with yourself, and use common sense:

- Look at your take-home pay (after taxes, after tax-deferred retirement contributions)

- Add up all of your other debt (consumer/credit card, student loans, auto, etc.) and look at your monthly payments (Note: if you have high interest loans, stop here, use any extra cash to pay down these loans before looking to buy a home)

- Consider other priorities (Children: are you planning on having kids, will this affect your take home pay; Retirement: can you save more?)

- Figure out how much money you have for a down payment (you can always save more and wait before buying)

- Then, use a mortgage calculator (with adding in estimates for all of the costs mentioned above) to determine the amount you can afford

- Did I mention leave some cushion room in your monthly budget between income and all of your total monthly expenses

Readers, how did you figure out how much house you can afford?

I think it’s great you’re talking about this early on. I did this with an ex-girlfriend when we were thinking of buying a house. We started off listing everything we wanted….and we wanted EVERYTHING! By talking things out, we learned what we wanted and what we needed. We also learned what we would be OK without. If we didn’t talk about it, we might have ended up buying too much of a house and regretting it later.

Thanks. Yeah, my hope is that by talking about it now, we can save up money and avoid getting something that we don’t need.

We knew the max that we wanted to spend each month and arrived at our pricing that way. But when you do that, you need to make sure that you’re including taxes and insurance in the calculations, not to mention repairs and maintenance!

Also, I would really recommend another look at the 28-40% figure. That’s really high. Ours is currently at about 10% of our monthly take-home (after taxes, insurance, 401K contrib, etc…), and even when we were living off only 1 salary it was about 20% of take-home pay. Having it much higher might be a really big stressor if anything changes for the worse income wise as it’s not an easy expense to shave down or cut out (unlike gym memberships that you can cancel).

Thanks Mrs. Pop. You’re definitely an inspiration when it comes to real estate. I think 28-40% is accurate for us, but that’s because we live in the NE. We spend more in housing than most families, but we also spend less in transportation and other costs.

Great points. I think it’s great you’re looking at this now as opposed to when you’re house shopping. Thankfully we had really good mortgage lender who helped us decide and our mortgage payment is really not much more than our rent was and we were able to afford that, so it worked out well for us.

That is great! I’m glad to hear the lender helped you instead of trying to get more money our of you. 🙂

I’m not ready to buy a home yet, but I imagine I’ll just look at what I could afford in a monthly payment in my budget, without sacrificing other goals like retirement and travelling. The hardest part will be budgeting for taxes and maintenance, but I suppose doing as much research as possible beforehand will prepare me for that.

Doing as much research as possible has been my motto. I hope it works out for you Jordann.

We wanted to be under the 35% threshold when we bought our house. That was over 3 years ago and we were only 20 and made hardly anything! Now our house is less than 10% of our after-tax monthly income 🙂

That’s great Michelle. Maybe someday I’ll be below 10% if my wife keeps doing well with her career. 😉

We spent much less than we could afford. If you have a decent income in a low cost of living area it is much easier to do this. We have extra buffer in our budget because of it and it is a nice thing to have.

I think that’s a great way to go. It gives you a lot more flexibility instead of being strapped for cash. 🙂

We tended to look at the amount of gross monthly income to decide and go with that as well as a place that was big enough for the family. It did happen to stay within the annual salary rule also.

Nice – Thanks for sharing JT.

I’m glad to hear that you are prioritizing savings. Good luck saving up enough money!

Other factors when buying a home is sewer, water, garbage and higher utility bills than an apartment.

When we bought our house I insisted on a side rental attached to the house to help with the mortgage. Our priority is our retirement savings, so we budgeted for 30% of net income after maximizing both our 401Ks, not on gross income.

So many factors come into play when it comes to buying a house and I agree with you that it is important to sit down with your wife or partner in order to come up with the best plan and budget. This article is really great for first time home buyers.

I think the best thing my husband and I did when we were first starting our house hunt was to figure out what we were comfortable paying before we even got pre-approved. I didn’t want to be tempted by what the bank was WILLING to lend us, because I knew it would be higher than our comfort zone.

The house we wound up with is well within the traditional rules: purchase price was just over double our yearly income and payments – including taxes and insurance – are 27% of our NET income, with no credit card debt and minimal student loan payments. Good thing, too. We planned on only having one car payment at a time, but the transmission in my husband’s car decided to go an die on us, and it would cost more to fix it than the car is worth. We opted to put that money toward a downpayment for a newer, more reliable car, which means now we have TWO car loans in as many months. If we’d reached toward the upper limit of the “traditional” rules, we might not have had the cash savings for a downpayment, OR the wiggle room in our budget to afford 2 car payments at once. (I just bought a car in Sept.)

Moral of the story: Live below your means!!

I actually have quite a number of posts about purchasing our first place. We live in a big (read: expensive) city and we wanted to move up in the world. We can’t afford a house here so we just had little things we wanted: a second bedroom, an outdoor space, etc. It would have upped our payments a few hundred dollars a month (which we could afford.) Yeah, I am talking about buying a co-op in a building.

But then after realizing that none of these places are places I see myself loving or living in forever, we just focused on getting something similar to what we have now, making somewhat of an investment and actually paying less than our current rent when you include everything.

We recently bought our first house and it has a pretty cool setup with a studio apartment in the basement with it’s own walkout so that it can be completely seperate from the rest of the house. We don’t plan on having kids for probably 7 years or so, and the house we bought has a few positive things about it:

1 – The rental unit is big as we will be spending a couple hundred less per month than we were paying as renters, even after utilities are considered. There is always the risk that it will lie vacant but I think that risk is small since we had a number of people interested before we even closed on the house, and that was just from casual conversations with friends with no intention of “marketing” the rental to them or whatnot. We also can afford the mortgage without the rental income, which is an obvious plus.

2 – As I said, we don’t plan on having kids which helps with the finances, as you mentioned above. The upstairs and basement, plus the yard and garage, are more than enough space for us right now. If we did ever need more space, the rental unit could be converted into more living space.

3 – We found a house that was not staged, had some outdated features, and could use some work. Because of this, we were able to get the house for a lot less than they were initially offering. Honestly, if they had spent $3-$20k on cosmetic fixes and upgrades, they could have easily gotten what they originally listed the price as. Most of the fixes are very inexpensive, like painting, replacing blinds, replacing vents, replacing light switches, removing wallpaper, etc. Again, the combination of having a renter and not having kids will allow us to put the time and money towards small fixes over time so that when we go to sell it we will hopefully make a profit.

Anyway, it’s awesome that you are factoring in all the variables. I recently wrote a post about 10 expenses to consider when buying a home and it touches on some of the things people don’t generally think about. Check it out if you have a few minutes – http://www.youngadultmoney.com/2012/10/22/10-expenses-to-consider-when-buying-a-home/